Options pricing explained

What you actually pay for — intrinsic vs extrinsic value, and the forces that move an option's premium.

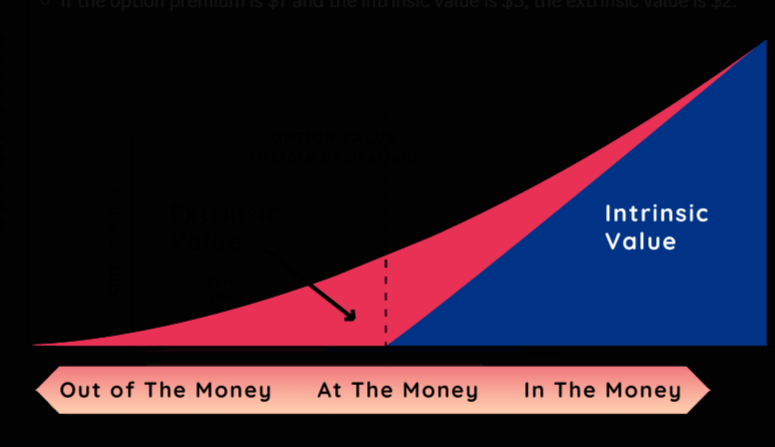

Intrinsic value

An option's price — its premium — comes from two parts. The first is intrinsic value: what the option is worth if you exercised it right now.

Call intrinsic value = max(0, current price − strike). Put intrinsic value = max(0, strike − current price).

Example: a stock at $55 with a $50-strike call has $5 of intrinsic value ($55 − $50).

Extrinsic (time) value

The second part is extrinsic value, also called time value — the extra you pay for the time left and the market conditions.

Extrinsic value = premium − intrinsic value.

Example: if the premium is $7 and the intrinsic value is $5, the extrinsic value is $2.

What moves an option's price

Option prices come out of pricing models like Black-Scholes. Several inputs push the premium up or down at the same time.

The key factors

Here's how each one works:

- Time to expiration — more time means more extrinsic value; as expiry nears, that value bleeds away (theta decay). A 3-month call might cost $10 where a 1-week call on the same strike costs $2.

- Volatility — implied volatility (IV) is the market's expectation of future swings; higher IV means richer premiums. A biotech before an FDA decision has far pricier options than a stable utility.

- Underlying price — the closer the asset trades to the strike, the more extrinsic value. A $50-strike call is worth more with the stock at $49 than at $40.

- Interest rates (rho) — higher rates tend to lift call values and weigh on puts.

- Dividends — stocks paying big dividends often have cheaper calls, since the price usually drops after the payout.

Putting it together

Stock ABC trades at $60. You're looking at a $55-strike call, expiring in a month, priced at $8.

Intrinsic value = $60 − $55 = $5.

Extrinsic value = $8 − $5 = $3.

That $3 is what you're paying for the time left and the chance the stock climbs further.

Final thoughts

Knowing what makes up a premium — and what moves it — is what separates guessing from strategy. Time decay, volatility and the rest all pull on the price at once.

Next: the Greeks, which measure exactly how sensitive an option is to each of these factors.

Educational content — not financial advice.